You notice the crack first because the afternoon light catches it. Then you see the skirting has pulled away, a door no longer closes properly, and the waterproofing issue you hoped was minor clearly isn’t. You call the builder and get silence, or worse, discover the company has gone under. At that point, most homeowners aren’t thinking about legal categories or evidentiary standards. They want to know one thing. Can this still be fixed without carrying the whole cost themselves?

That’s where hbcf claims assessments become important. In New South Wales, the Home Building Compensation Fund can provide a pathway when the right trigger event has occurred and the claim is properly prepared. But the process is not forgiving. The scheme is document-heavy, deadline-driven, and highly dependent on whether the defect is correctly identified, classified, and costed from the start.

Your Guide to Navigating HBCF Claims Assessments

A lot of owners come to this process after months of stress. The build may already be incomplete, or the work was finished but serious defects have now appeared. By the time they start asking about HBCF, they’re usually dealing with two problems at once. The first is the building issue itself. The second is proving it in a way the insurer and any later tribunal process will accept.

That second problem catches people out.

In the 2018 to 2019 financial year, HBCF claims in NSW rose from 769 to 928, which was a 20.7% increase, and 72% of the $49 million in gross claim payments related to major defects according to the NSW Home Building Compensation Scheme report. That tells you something practical. A large share of these claims turns on serious defect issues, and serious defect issues rarely succeed on vague descriptions and rough quotes.

Where owners usually go wrong

The most common mistake isn’t that the defect doesn’t exist. It’s that the owner starts with the wrong material. They rely on a short builder’s quote, a few mobile phone photos, and an email chain full of understandable frustration but very little technical substance.

Practical rule: If the claim may be scrutinised by an assessor, a loss adjuster, or later by NCAT, the evidence needs to explain cause, scope, defect classification, and rectification method. Not just price.

That’s also why outside insurance material can still be useful for mindset, even where the scheme is different. The Four Seasons Roofing insights on claims are a useful reminder that insurers assess evidence, causation, and repair scope closely. HBCF is no different in that respect.

What actually helps

A strong HBCF claim usually starts with four things:

- A clear trigger event: You need to confirm that the claim sits within the scheme’s requirements.

- Correct defect classification: Major and non-major defects don’t follow the same limitation periods.

- Proper technical evidence: The report has to do more than say work is poor.

- Reasonable rectification costing: The scope and pricing must line up with the actual defect.

When owners or solicitors engage a consultant early, the whole claim tends to become easier to manage. Dates get pinned down. The defect list becomes organised. The claim shifts from a distressed narrative to a supported technical case.

Understanding Your HBCF Coverage and Eligibility

HBCF is not a general maintenance policy and it isn’t a substitute for every building dispute pathway. It operates as a last-resort form of protection when the statutory trigger has occurred, and whether you’re inside time depends heavily on the type of claim.

Why classification matters immediately

The biggest issue at the start is often misclassification. A defect may look cosmetic to a layperson but can involve non-compliance, water ingress, movement, structural distress, or systemic failure. On the other hand, some owners assume every defect is major when the available evidence doesn’t support that position.

The distinction matters because the limitation periods differ. The HBCF coverage overview notes that major defects have a 6 year limitation period from completion, while non-major defects have a 2 year limitation period. It also notes that misclassifying a defect can leave a claim out of time.

A consultant’s job at this stage isn’t to dramatise the defects. It’s to classify them properly and explain the technical basis for that classification.

HBCF claim types and time limits

| Claim Type | Time Limit from Work Completion | Coverage Details |

|---|---|---|

| Major defects | 6 years from completion | Repair cost recovery for defects properly classified as major |

| Non-major defects | 2 years from completion | Recovery for covered defects that do not meet the major defect threshold |

| Inability to complete work | Within 12 months of work discontinuation | Limited category for incomplete works, subject to scheme requirements |

| Failure to commence work | Within 1 year from failure to commence | Can address deposit-related loss in the relevant circumstances |

A few practical points follow from that table.

- Completion dates matter: Don’t guess. Get the contract, occupation documents, certificates, and any correspondence that helps establish when the relevant work was completed.

- Discovery dates matter too: If a defect was identified late, the timing of awareness can become important.

- Incomplete work is different from defective work: Owners often blend the two together. The insurer won’t.

The first eligibility check

Before spending money on full claim preparation, confirm three things:

- There is an HBCF certificate tied to the residential building work.

- The claim category fits the facts as they stand.

- The time limit hasn’t expired.

If you’re dealing with a Crown or grant-related issue alongside home building compensation questions, the background on Home Building Compensation Fund grants from the Crown can help frame part of that broader context.

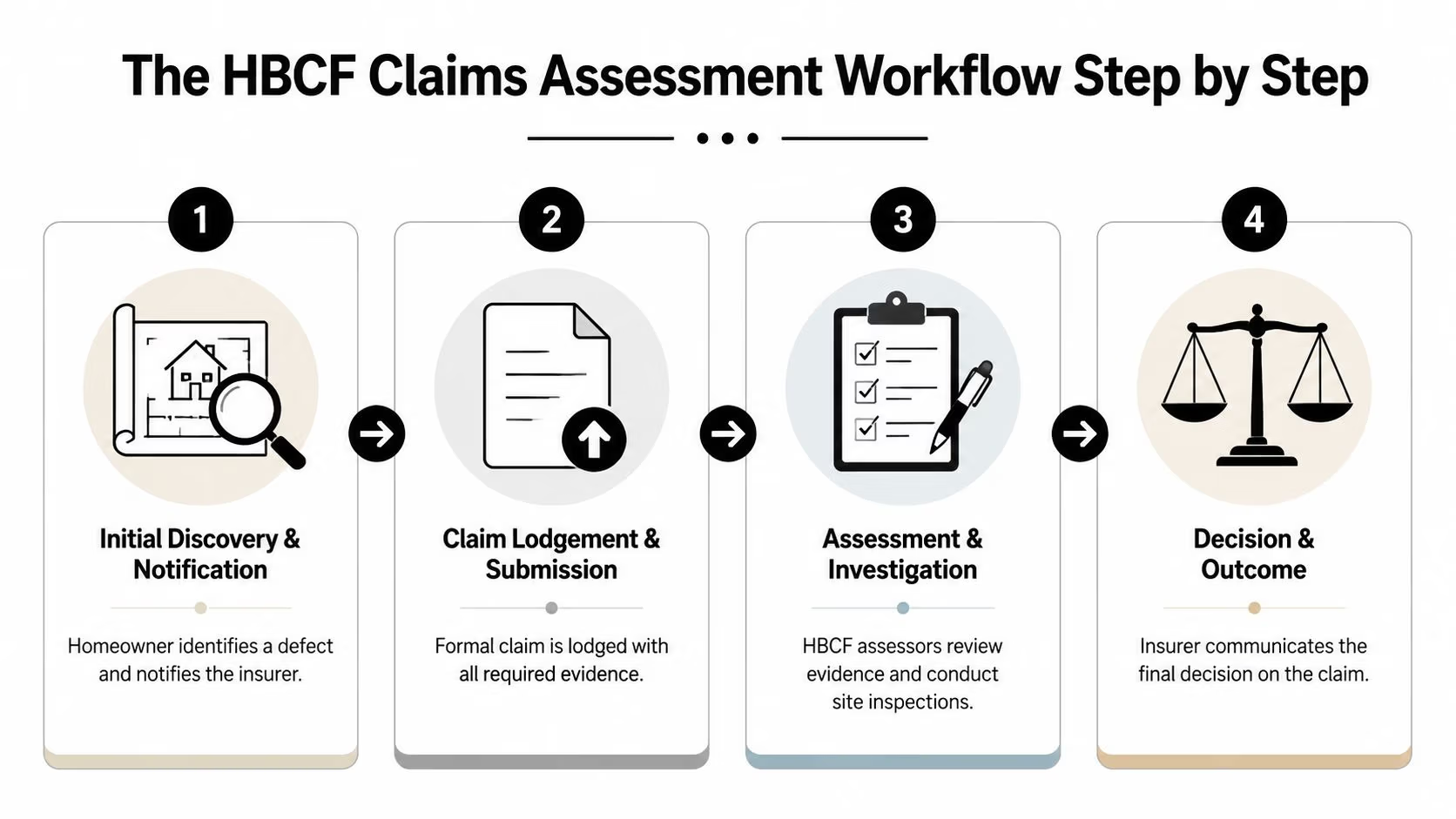

The HBCF Claims Assessment Workflow Step by Step

Owners often think the claim starts when they submit a form. In practice, the process starts earlier, at the moment they become aware of the builder’s insolvency or other relevant trigger. That’s when timing becomes critical.

The NSW HBCF claims process summary states that homeowners must notify NSW Fair Trading within 30 days of becoming aware of a builder’s insolvency, and once the claim is formally lodged, there is a 90-day determination period during which the evidence and the reasonableness of rectification quotes are assessed.

Step one: protect the dates

The first thing I tell clients is simple. Build a date file before you build an argument.

Include:

- The date you became aware of the builder’s insolvency: Keep the email, ASIC extract, letter, or other document that shows when and how you learned of it.

- The notice to Fair Trading: Keep a copy of what was sent and when.

- The dates of defect discovery: This is separate from builder insolvency and can matter for classification and limitations.

If the dates are unclear or inconsistent across your documents, the claim starts on weak footing.

Step two: lodge with a proper evidence set

A formal claim should not be treated like a placeholder if avoidable. It should be accompanied by coherent material that lets the assessor understand what went wrong, where it is, why it matters, and what it will take to rectify.

That usually includes:

- Contract and policy documents

- Photographs and site records

- Reports identifying the defects

- Quotes with itemised scope, licence details, and clear cost breakdowns

Many owners lodge early and try to fix the evidence later. Sometimes that works. Often it leads to confusion, repeated requests, and preventable disagreement about scope.

Step three: expect scrutiny during assessment

During the assessment period, the insurer or appointed representatives will review whether the claim falls within cover and whether the quoted rectification costs are reasonable. That means they are not merely checking whether damage exists. They are also testing whether the proposed repair methodology and cost align with the defect and the policy response.

If a quote says “repair bathroom waterproofing” with one lump sum, that’s usually not enough. The assessor wants to see what is being demolished, what is being reinstated, what standards are implicated, and who is performing the work.

Step four: read the determination carefully

The determination letter matters as much as the original claim. It can approve the full amount sought, approve a reduced amount, or reject parts of the claim. Reductions often arise because the quoted work is considered excessive, unsupported, or not attributable to the insured event.

When that happens, don’t react emotionally first. Read the reasons line by line. Work out whether the issue is one of timing, classification, causation, scope, or cost substantiation. Those are very different problems and they require different responses.

Essential Evidence for a Successful Claim

An HBCF claim succeeds or fails on the quality of its evidence. Owners often think a quote proves the defect. It doesn’t. A quote proves that someone is willing to perform work for a price. It does not necessarily prove the nature of the defect, its extent, its cause, its classification, or that the proposed rectification is the appropriate response.

A quote is not the same as expert evidence

A contractor’s quote can be useful, especially where it is itemised and prepared by the right licensed trade. But for contested or technically involved claims, it is only one part of the file.

A proper expert report should usually deal with:

- Location of each defect: Room by room, element by element.

- Description of the observed condition: Cracking, moisture ingress, out-of-plumb framing, membrane failure, movement, incomplete work, or other issue.

- Reference points: Relevant drawings, approvals, specifications, Australian Standards, tolerances, and accepted building practice where applicable.

- Causation analysis: What likely caused the issue, and whether it is consistent with defective workmanship, design, incomplete work, or another source.

- Rectification pathway: What needs to be done to remedy it.

That is why solicitors often seek an Expert Witness Report rather than relying on trade quotes alone.

What assessors and lawyers need to see

Good evidence is organised. It doesn’t bury key findings in long narrative or force the assessor to guess how one defect connects to one cost item.

The strongest files usually include:

- A defect schedule that identifies each issue distinctly.

- Annotated photographs showing scale, location, and progression where relevant.

- A reasoned expert opinion tying the observed defect to technical non-compliance or defective work.

- Rectification quotes that mirror the defect schedule rather than using broad lump sums.

“If the evidence can’t be mapped defect by defect, the claim becomes harder to assess and easier to cut down.”

Where a Scott Schedule helps

When multiple defects are in issue, or where the matter may proceed into litigation or NCAT, a Scott Schedule becomes very useful. It lets each alleged defect be listed in a structured format with corresponding responses, opinions, and rectification items. That cuts through the usual confusion of mixed emails, competing reports, and overlapping scopes.

For many disputes, that structure becomes more valuable than people expect. It forces precision. It also exposes weak items early, which is better than discovering them after the other side has challenged the report.

One available option for this kind of documentation is Awesim Building Consultants, which prepares site investigation material, Expert Witness Reports, and Scott Schedules for residential building disputes and HBCF-related matters.

Common Reasons HBCF Claims Are Rejected

The assessment environment in NSW is strict for a reason. A 2020 independent review of the HBCF found that average claim values in NSW are around 50% higher than comparable schemes in Victoria and Queensland. Where claim values are higher, scrutiny tends to be heavier. Every part of the file is more likely to be tested.

The avoidable failures

Most rejected or reduced claims fall into a handful of patterns.

- Missed deadlines: The owner waits too long after learning of insolvency or acts too late on limitation issues.

- Weak classification: The defect is labelled major without a sound technical basis, or a major defect is treated too casually until time becomes a problem.

- Poor evidence: The material shows dissatisfaction but not a persuasive technical case.

- No proper trigger event: Owners assume HBCF applies solely because there is defective work.

- Unreasonable costings: The repair scope is inflated, vague, duplicated, or unsupported.

Each of those problems can be prevented, but not with guesswork.

What works better in practice

The better approach is disciplined and a bit less emotional.

Start with documents, not assumptions

Pull the certificate, contract, plans, approvals, occupation documents, progress records, emails, and any insolvency material. If a critical date cannot be supported, find out early rather than after submission.

Separate each defect

Don’t write “the house is defective” and hope the detail will emerge later. List each issue as its own item. Cracked slab, failed waterproofing, balcony falls, roof water ingress, external cladding defects. Separate items are easier to inspect, classify, and cost.

Match the quote to the defect

If the report identifies a membrane failure in one wet area, the quote shouldn’t read like a full house renovation unless there is a technical basis for that scope.

Claims often fail because the owner is right about the defect but wrong about the way it has been documented and costed.

The hidden problem of mixed-purpose reports

Another common issue is using a report prepared for a different purpose. A pre-purchase inspection, a maintenance note, or a builder’s variation email might be useful background, but it usually won’t answer the insurer’s key questions. HBCF claims assessments need evidence suited to classification, causation, and rectification.

That’s why the file should be built for the claim you are making, not assembled from whatever paperwork happens to already exist.

Engaging a Building Consultant for Your Claim

By the time a homeowner calls a consultant, the matter has often become personal. They’ve spent money, lost trust, and now have to turn a lived problem into admissible evidence. That is hard to do alone, especially when the defects involve multiple trades or there’s already disagreement about what is defective and what is merely incomplete.

What a consultant actually does

A building consultant doesn’t just inspect and write a few pages. In a proper HBCF matter, the role is broader.

- Investigate the site carefully: Not just visible defects, but likely cause, spread, related building elements, and practical rectification implications.

- Prepare structured technical evidence: A report should identify each defect, the supporting observations, and the likely rectification method.

- Organise complex disputes: If there are many items or legal proceedings are likely, a Scott Schedule can bring discipline to the whole case.

- Help the legal team focus: Lawyers need clear technical opinions. They don’t need a report that wanders or overreaches.

Why experience matters here

In construction disputes, theory on its own isn’t enough. A consultant needs enough site experience to recognise what is happening in the building, what trades are involved, what parts must be opened up, and which apparent defects are symptoms of a deeper problem.

That practical background makes a difference when assessing whether an item is superficial, systemic, caused by sequencing failures, or connected to non-compliant workmanship. It also matters when reviewing contractor quotes. Some scopes are realistic. Others are padded, incomplete, or technically unsound.

If you need technical input before lodging, or if your solicitor needs independent support for an existing matter, get advice from a consultant who works in residential defects, expert reporting, and dispute documentation regularly.

Frequently Asked Questions on HBCF Claims

Is an HBCF claim the same as a statutory warranty claim

No. They can overlap factually, but they aren’t the same pathway. If the builder is still trading and can be pursued directly, statutory warranty rights may be central. HBCF is generally engaged when the relevant last-resort trigger exists.

Is the insurer’s loss adjuster enough on its own

Not usually from the owner’s perspective. The loss adjuster is part of the insurer’s assessment process. An independent consultant’s report serves a different purpose. It documents the owner’s technical case, supports classification, and can be used more broadly if the dispute continues.

Do I need a Scott Schedule for every matter

No. Some smaller claims can be managed without one. But where there are multiple defects, competing positions, or likely tribunal proceedings, it can save substantial time and reduce confusion.

Will every proven defect be paid in full

Not necessarily. Even where a defect is accepted, the insurer may still examine whether the proposed rectification cost is reasonable and whether each item falls within the scope of cover.

If you need help preparing evidence for an HBCF matter, Awesim Building Consultants can assist with site investigations, Expert Witness Reports, and Scott Schedules for homeowners, solicitors, and other parties dealing with residential building disputes. Email admin@awesim.com.au or call 1800 293 746.