You’ve found defects, the builder has stopped responding, and every phone call seems to create a new layer of confusion. That’s usually the point where homeowners and solicitors start looking into home building compensation fund claims assessments in NSW, only to realise the process is far more technical than the basic summaries suggest.

The HBCF can be a genuine safety net, but it isn’t a general dispute-resolution scheme and it doesn’t reward vague complaints. It responds to particular trigger events, strict notification periods, and evidence that can stand up to insurer scrutiny and, if necessary, NCAT review. The practical difference between a weak claim and a strong one often comes down to timing, classification of the defects, and whether the documents prove cause, scope, and rectification cost.

Your Guide to HBCF Claim Assessments

This issue often arises at the worst possible time. The house is unfinished, or the defects are getting worse, and the builder may be insolvent, missing, or beyond practical reach. At that stage, broad statements like “the work is defective” don’t help much. What matters is whether the problem fits the HBCF framework and whether the claim is prepared in a way an assessor can act on.

The HBCF is designed as a last-resort protection. That means the assessment process is formal, document-heavy, and built around proof. Homeowners often assume that obvious defects will speak for themselves on inspection. In practice, they rarely do. The assessor needs to see what the defect is, why it matters, when it arose, whether it falls within the policy period, and what it will reasonably cost to rectify.

What usually decides the outcome

A claim tends to turn on a handful of practical points:

- The trigger event is valid: builder insolvency, disappearance, death, or another recognised event must be established.

- The defect category is correct: major and non-major defects have different time limits.

- The evidence is organised: contract documents, plans, photos, correspondence, expert reports, and rectification costings all need to line up.

- The narrative is coherent: the documents should tell one consistent story from contract through to damage and loss.

The strongest claims don’t just list problems. They show the assessor exactly what happened, what standard was breached, and what work is needed to fix it.

There’s also a practical overlap with broader HBCF entitlement issues, particularly where policy responses and recovery pathways become contested. For background on that side of the scheme, it can help to read about HBCF grants from the Crown.

Why homeowners get stuck

Public information usually explains when a claim might exist, but not how to build one properly. That gap matters. If the materials lodged at the start are incomplete, inconsistent, or technically weak, the assessment can narrow quickly and become much harder to correct later.

A good claim file works like a construction brief, not a complaint letter. It should let an assessor or tribunal member follow the issues item by item without guessing.

What Triggers an HBCF Claim Assessment

An HBCF claim assessment doesn’t begin just because a dispute exists. A builder can do poor work, delay the job, or argue about variations, and none of that automatically opens the fund. The scheme is meant to respond when the builder can’t meet their obligations and the claim falls within one of the recognised trigger events.

The usual trigger events

Common triggers include:

- Insolvency: the builder enters liquidation, administration, or another form of insolvency that prevents completion or rectification.

- Disappearance: the builder can’t be located after reasonable enquiries.

- Death: relevant where the builder was an individual and the work can’t be completed or rectified through the business.

- Licence suspension linked to non-payment of an order: this can arise where a builder fails to comply with a court or tribunal order to pay money.

For insolvency-related matters, the assessment isn’t just administrative. It becomes a financial and forensic process, and claims are claimable within 12 months of cessation. They can cover up to 100% of completion costs, capped at the policy limit. In the same context, data from icare’s administrator states that defect claims constitute about 60% of all payouts, with structural failures supported by detailed engineering reports yielding the highest recoveries for homeowners, as discussed in Contracts Specialist’s overview of icare’s role in administering HBCF.

What doesn’t trigger the fund

A few situations regularly cause confusion:

| Situation | HBCF trigger by itself |

|---|---|

| Builder is slow to respond | No |

| Builder disputes scope or cost | No |

| You’re unhappy with workmanship but builder is still trading and available | Usually no |

| Builder has become insolvent or cannot be found | Potentially yes |

That distinction matters because many owners spend months arguing about defects without first confirming whether the fund can even be engaged.

If there’s no valid trigger event, the quality of your defect evidence won’t rescue the claim.

Practical steps before lodgement

If you suspect a trigger event has occurred, gather proof immediately. That may include insolvency records, returned correspondence, licence information, unanswered emails, text messages, and a chronology of your attempts to contact the builder. “Reasonable efforts” should be visible on paper.

Solicitors often do this well when they prepare a clear timeline. Homeowners often don’t, because they assume the disappearance or collapse is obvious. It may be obvious to you. It still needs to be proved to the insurer.

Understanding Claim Timelines for Defects

Timing is one of the most unforgiving parts of home building compensation fund claims assessments. If the defect is notified outside the applicable period, the claim can fail even where the building problem itself is real and serious.

Major defects and non-major defects

The law draws a hard line between major defects and non-major defects. Major defects are claimable for up to 6 years and affect structural integrity or weatherproofing. Non-major defects are limited to a 2-year claim period. Failure to notify within those policy periods is a primary cause of claim denial and accounts for a significant portion of rejections, as explained in Etheringtons’ HBCF guidance.

That sounds straightforward until you apply it to real buildings. Owners often describe everything as “major” because the consequences feel major to them. But the classification turns on the legal and technical nature of the defect, not the owner’s frustration.

A practical way to think about classification

Use this as a working guide:

- Likely major defects: footing movement, slab failures, significant water ingress through the building envelope, serious structural cracking, defects affecting safety or habitability.

- Usually non-major defects: finish problems, minor alignment issues, isolated cosmetic cracking, paint defects, sticking doors where the issue doesn’t stem from a major structural failure.

That doesn’t replace a proper inspection. It does show why early expert input matters. A defect that looks cosmetic can sometimes be the visible symptom of a larger structural or waterproofing issue. The reverse is also true. Owners sometimes spend too long treating a non-major issue as if it can be dealt with later.

Don’t wait for the defect to become dramatic. The legal clock usually starts from completion, not from the day the problem became impossible to ignore.

What to do if you’re close to the deadline

If the dates are tight, act in this order:

- Confirm the completion date from the contract, occupation certificate, practical completion documents, or related records.

- Record the defects immediately with dated photos and notes.

- Obtain an expert assessment that classifies the issues properly and ties them to the relevant standards.

- Notify within time even if some of the supporting material is still being finalised.

A lot of owners lose time trying to make the file perfect before lodging. In a time-sensitive matter, preserving your position matters more than producing a polished package on day one.

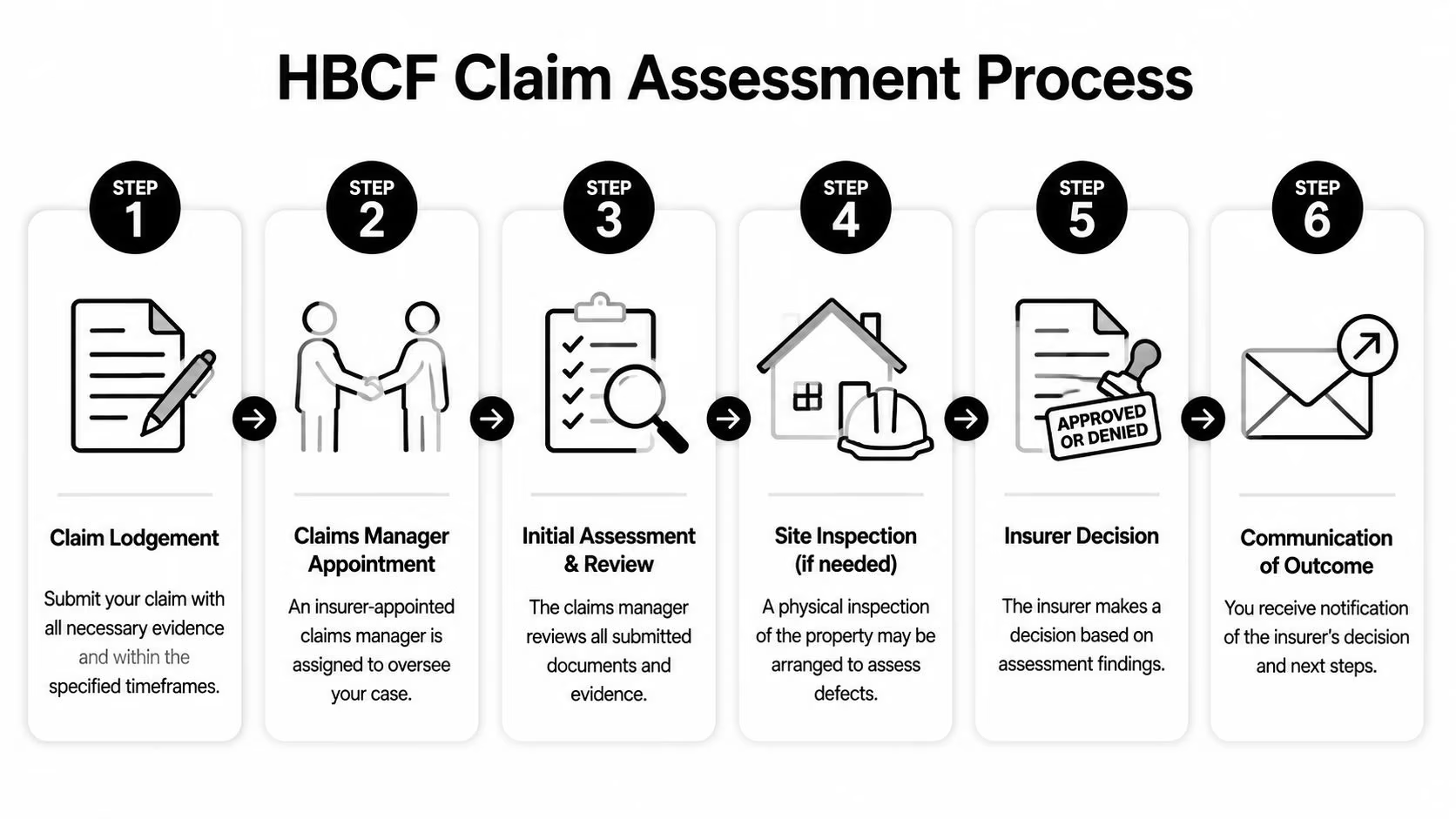

The HBCF Claim Assessment Process Step-by-Step

Once the claim is lodged, the process becomes procedural. The insurer or its appointed claims manager works through coverage, trigger event, scope, and valuation. If your file is disorganised, the assessment often slows down at the very stage where clarity is needed most.

The six practical stages

Claim lodgement

The owner submits the claim, ideally with the contract, plans, payment records, defect evidence, correspondence, and any expert material already available.Claims manager appointment

The claim is allocated for handling. At this stage, the administrative discipline of your file starts to matter.Initial review

The reviewer checks whether there is an active policy, whether a valid trigger event appears to exist, and whether the matter is within time.Site inspection

If the matter requires it, an inspection is arranged. That inspection is important, but it shouldn’t be the first time the technical case is explained.Assessment of scope and cost

The assessor considers which items fall within the policy response and what rectification or completion cost is supported.Decision and communication

You receive an outcome. It may be accepted, partly accepted, or declined.

What assessors are usually looking for

In practical terms, the assessor is testing several things at once:

| Assessment issue | What helps |

|---|---|

| Is the claim eligible? | Trigger event evidence and policy details |

| Is it in time? | Reliable completion date and prompt notification |

| Is the defect covered? | Clear identification of each defect and its category |

| What is the cost? | Itemised scope and reasoned rectification costings |

Serious defect work plays a significant role in assessment. In the 2018-2019 financial year, the HBCF paid $49 million in gross claims, with 72% or $35 million attributed to major defects and 18% or $9 million to incomplete work, according to the SIRA Home Building Scheme Report for 2018-2019. That tells you where the scrutiny often falls. Major defect claims are prominent, technical, and expensive.

What works and what usually fails

What works is simple, even if it takes effort:

- A coherent chronology

- Defect descriptions tied to standards or contract requirements

- Photos linked to specific items

- Costings that explain scope, not just totals

What fails is equally predictable:

- A bundle of emails with no index

- Photos with no dates or room references

- Quotes that don’t describe the actual rectification method

- A claim lodged on urgency alone

If you’re dealing with loss quantification or disputed scope, it also helps to understand the broader issue of HBCF losses and how they’re framed.

Essential Evidence for a Strong Claim Submission

A weak HBCF file reads like this: there are lots of defects, the builder has been difficult, and the owner is understandably upset. A strong file does something different. It identifies each issue, locates it, explains the defect, links it to a breach, and gives the assessor a rational basis to cost the remedy.

That difference is why evidence matters more than volume. More documents don’t automatically create a stronger claim. The right documents, organised properly, do.

The documents that carry real weight

At minimum, the claim file should usually include:

- The building contract and variations: these establish the agreed scope and any changes.

- Approved plans and specifications: without them, it’s harder to show what should have been built.

- Payment records: these help with incomplete works claims and sequencing of events.

- Correspondence trail: emails, texts, letters, notices, and requests for rectification.

- Photographs and video: dated, room-by-room, defect-by-defect, and wide enough to show context.

- Independent reports and costings: with these, most claims become materially stronger.

Why expert material changes the file

There is a significant public information gap around the specific criteria and qualifications of HBCF assessors. That uncertainty leaves many owners guessing about what the assessor will require. Preparing a claim with NCAT-compliant Scott Schedules and Expert Witness Reports, which provide verifiable defect quantification up to the $340k policy cap, directly addresses that problem by giving the assessor objective material to work with, as discussed in Schimann’s article on understanding HBCF.

An expert report does three things a complaint letter can’t:

- Classifies the defect properly

- Links the issue to relevant building requirements or standards

- Sets out a reasoned rectification approach

A Scott Schedule becomes especially useful when there are multiple defects or a live NCAT dispute. It forces the case into item-by-item form. That’s often the first time the dispute stops being emotional and starts becoming manageable.

A Scott Schedule is valuable because it turns “the whole job is defective” into a list of precise, answerable items.

What evidence is often overrated

Homeowners sometimes focus too heavily on:

- Long narrative emails

- Screenshots without dates

- Verbal statements from trades who won’t sign a report

- Lump-sum quotes with no scope breakdown

Those materials can support the story, but they usually won’t carry the case on their own.

A better way to assemble the file

Treat the claim like a brief for someone who has never seen the house. Put the documents in order. Label every photo. Number each defect. Match each defect to a room or elevation. Keep the chronology separate from the technical report so both can be read quickly.

That sounds basic. It also solves a large share of the practical problems seen in disputed assessments.

Navigating Disputes and NCAT Proceedings

A claim outcome isn’t always the end of the matter. Owners regularly disagree with the insurer’s decision on scope, causation, valuation, or outright denial. When that happens, the dispute usually shifts from “what happened on site” to “what can be proved.”

Where disputes usually arise

The common pressure points are:

- The defect is accepted, but the scope is too narrow

- The cause of the defect is disputed

- The rectification cost allowed is too low

- Some items are treated as maintenance or excluded work

- The claim is declined on timing or eligibility grounds

The financial stakes in NSW are high. An independent review found that average HBCF claim values in NSW are approximately 50% higher than in comparable schemes in Victoria and Queensland, even after adjustments. That finding appears in the independent review of the efficiency and effectiveness of the NSW HBCF. In practical terms, that means disputes over scope and valuation aren’t minor bookkeeping arguments. They can materially change the result.

Internal review first, then NCAT

A sensible progression usually looks like this:

- Request the insurer’s reasons clearly and in writing

- Identify the exact points of disagreement

- Provide targeted expert response material

- Seek internal review if available

- Move to NCAT if the dispute remains unresolved

NCAT changes the environment. Once you’re there, broad dissatisfaction won’t get much traction. The tribunal will want structured evidence, a clear defect list, and opinions that can be tested.

In NCAT, the better organised party often appears more credible before anyone even reaches the technical merits.

Why contract administration still matters

Many HBCF disputes sit on top of older contract problems. Incomplete records of progress payments, variations, and milestones can muddy the assessment of loss or completion cost. For solicitors and owners trying to tighten up that side of a building dispute, Redline’s guide on payment terms is a useful reference because payment structure and documentary discipline often become relevant long before the insurance issue appears.

What expert witnesses actually contribute

A proper expert witness doesn’t just repeat the owner’s grievances. The expert should isolate the defects, explain causation, separate consequential damage from original defective work, and justify the rectification method. That’s particularly important where the insurer’s assessor has taken a narrower view.

At tribunal level, credibility comes from method. Clear inspection notes, standards-based reasoning, measured language, and an itemised schedule usually carry more weight than forceful assertions.

How Awesim Building Consultants Strengthens Your Claim

When an HBCF claim turns contentious, technical clarity becomes the difference between momentum and drift. Homeowners often know something is badly wrong but struggle to present it in the form insurers, solicitors, and tribunals need. Lawyers may understand the procedural path but still require independent building evidence that is clear, measured, and properly itemised.

That’s where a specialist building consultant adds value. The role isn’t to dramatise the defects. It’s to document them accurately, classify them properly, and produce evidence that can survive scrutiny.

What Awesim provides

Awesim Building Consultants brings 35+ years in building and construction and 15+ years providing litigation support to homeowners, builders, and lawyers across NSW. The focus is on evidence that works in real disputes, not generic commentary.

Core services include:

- Site investigations that identify and document the actual building issues on the ground

- Expert Witness Reports prepared for building disputes and tribunal or legal proceedings

- Scott Schedules structured for NCAT use and item-by-item defect analysis

Why that matters in practice

A claim usually gets stronger when the evidence answers five practical questions cleanly:

| Question | Evidence that helps |

|---|---|

| What is defective? | Site observations, photographs, itemised defect list |

| Why is it defective? | Reference to standards, construction requirements, or contract documents |

| Where is it located? | Marked plans, room references, elevations, labelled images |

| What is needed to fix it? | Rectification methodology and scope |

| What will that cost? | Reasoned costing tied to the scope, not a bare lump sum |

That style of reporting helps at every stage. It helps before lodgement, during assessment, and later if the matter moves into dispute.

Good expert evidence reduces room for assumption. That helps the homeowner, the solicitor, and the decision-maker.

Who this support is for

The work is relevant to:

- Homeowners dealing with defective or incomplete residential work

- Solicitors preparing or responding to NCAT and related proceedings

- Builders and respondents who need independent assessment of alleged defects

- Insurers and loss adjusters requiring technical building input

If you need practical help with inspections, reports, or Scott Schedules for an HBCF or NCAT matter, getting the evidence right early usually saves time later.

If you need help from Awesim Building Consultants with a site investigation, Expert Witness Report, or NCAT-compliant Scott Schedule, contact the team for a confidential discussion. Email admin@awesim.com.au or call 1800 293 746.