Storm damage rarely arrives at a convenient time. You notice a ceiling stain spreading after heavy rain, a section of roof has lifted in high wind, or a crack that wasn’t there last month has opened through brickwork. The insurer asks for photos, a claim number is issued, and suddenly you’re dealing with assessors, scope of works, policy wording, and repair language that most owners only see when something has already gone wrong.

That’s where many claims start to drift. The owner is focused on getting the home secure and repaired. The insurer is focused on assessing liability under the policy. Those are related tasks, but they’re not the same task. If the cause, extent, or repair method is disputed, the gap between those two positions can become the whole case.

Your Guide to Navigating Insurance Claim Assessments

Most owners come to a building insurance claim under pressure. Water is coming in, plaster is swelling, flooring is lifting, and someone wants an answer immediately about what’s covered and what isn’t. The first few days matter because decisions made in a rush often shape the rest of the claim.

Property damage claims are common. In 2023, property damage including theft accounted for 97.3% of homeowners insurance claims, and the average settlement ranged from about $13,804 to $17,059 according to these homeowners insurance claim statistics. That matters for one reason. You’re not dealing with an unusual event, but you are dealing with a process that can still go off track if the evidence is poor or the scope of damage is narrowed too early.

A typical NSW owner starts by thinking the claim is straightforward. A storm hits, the insurer sends someone out, repairs are approved, end of story. Sometimes that’s exactly what happens. Sometimes the assessor says the visible damage is minor, the insurer treats the issue as maintenance rather than insured damage, or the repair scope ignores the underlying cause of the failure.

Practical rule: Treat the first inspection as the beginning of the evidence file, not the end of the problem.

Building insurance claims assessments work best when the owner understands two things early. First, the insurer’s process is driven by policy response, not by what feels fair on site. Second, if a dispute develops, you’ll need building evidence that stands up outside the insurer’s internal system.

Owners dealing with storm, water, impact, movement, or fire-related damage can get a clearer picture of the broader process through this guide to home insurance claims. It’s a useful starting point before the matter turns into a more formal dispute.

The Key Players in Your Building Insurance Claim

The claim process gets easier when you know who is doing what, and who each person is acting for.

The insurer and its appointed representatives

Your insurer makes the coverage decision. That sounds obvious, but many owners assume the site assessor has final authority. Usually, they don’t. They inspect, document, and report. The insurer then relies on that material, along with policy wording and internal claims handling.

An assessor or loss adjuster may attend the property. Their role can include inspecting damage, considering causation, reviewing what may be temporary versus permanent, and recommending a scope of works. They may be competent and thorough. But they are still appointed within the insurer’s claim process.

That distinction matters. Their brief is tied to the insurer’s file, the insurer’s instructions, and the insurer’s decision-making pathway.

For readers trying to understand the broader role of claim representatives, this explanation of what is a public adjuster is useful background. The terminology differs across jurisdictions, but the article helps owners understand why representation and independence matter in a property claim.

The builder, trades, and repair contractors

Repair contractors often enter the process before the dispute is fully understood. They may be asked to quote, make safe, or complete limited works. That can help stabilise the property, but it can also create problems if repairs start before the cause and extent of damage are properly recorded.

A contractor’s quote is not the same thing as a building opinion on causation. A repair price doesn’t answer whether damage was storm-related, pre-existing, progressive, or excluded under the policy.

A short overview of how claim discussions often unfold is worth watching before you respond to a disputed scope:

The independent consultant

An independent building consultant serves a different function. That role is to inspect the property, identify the relevant building issues, document defects or damage, consider likely causation from a construction perspective, and set out the repair scope in a way that can be tested.

The most important question isn’t who inspected first. It’s whose opinion is detailed, independent, and capable of surviving scrutiny when the claim is challenged.

If the insurer’s assessment aligns with the site conditions, an independent review may confirm that. If it doesn’t, the independent report becomes the basis for a proper challenge.

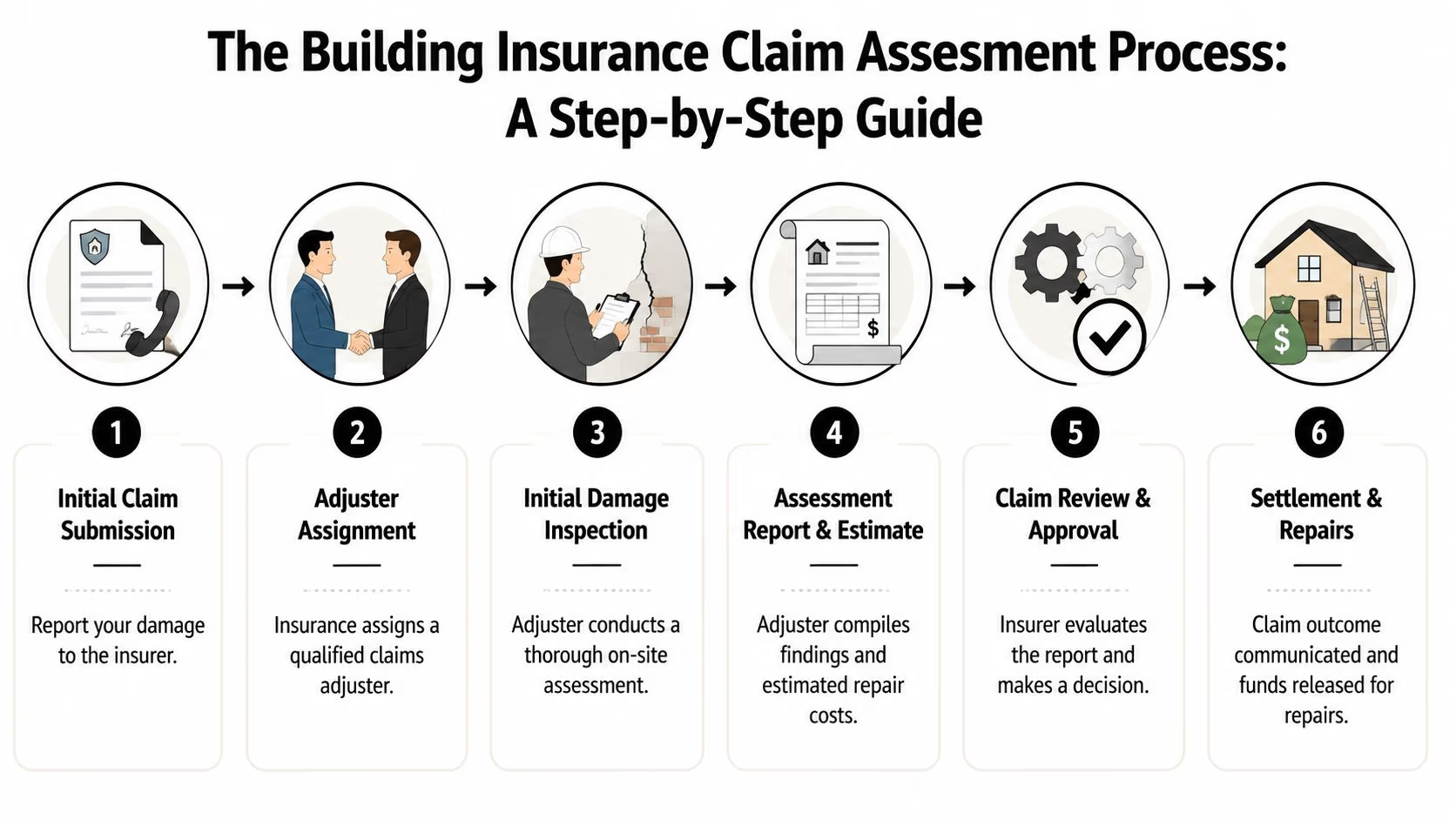

The Assessment Process and Timeline Explained

Most building insurance claims assessments follow the same broad path, even though timing varies from file to file. Delays usually come from incomplete information, access issues, questions about causation, or disagreement over repair scope.

What usually happens first

The process normally starts with the owner notifying the insurer and giving a short description of the event and visible damage. At that stage, keep the summary factual. State what happened, when you noticed it, and what areas are affected.

If there’s an immediate risk to safety or further deterioration, temporary make-safe work should be arranged. That can include tarping, isolating water ingress points, or preventing unsafe access. Keep records of who attended, what they did, and what they found.

The usual sequence on a live claim

Claim is lodged

The insurer opens the file and issues a claim reference. Owners should immediately create their own parallel file with photos, emails, invoices, notes of phone calls, and any maintenance records.Initial triage occurs

The insurer may ask for photos and a summary before deciding who to appoint. If damage appears limited, the claim can be desk-assessed at first. That’s one reason early photographs matter.Site inspection is arranged

The appointed assessor or adjuster attends. Be present if you can. Walk the entire affected area, not just the most obvious damage point.Further information is requested

This is common. The insurer may ask for plumber findings, roofer reports, historical photos, repair invoices, or details about when the damage first appeared.Scope and causation are reviewed

Disputes frequently arise during this stage. The insurer may accept some damage but not all of it. It may approve patch repairs where the owner says broader rectification is required.Decision is issued

The outcome may be approval, partial approval, request for more information, or denial. If accepted, the next issue becomes whether the approved scope effectively returns the building to the proper condition.

Where claims commonly slow down

A claim rarely stalls because one form is missing. It stalls because the file doesn’t clearly answer basic building questions.

| Claim stage | What helps | What causes delay |

|---|---|---|

| Initial lodgement | Clear event description and prompt reporting | Vague chronology |

| Inspection | Full site access and complete damage list | Only showing one room or one defect |

| Scope review | Independent trade or consultant input | Conflicting informal opinions |

| Final decision | Organised evidence and prompt responses | Missing maintenance or repair history |

Owners often expect one inspection to settle everything. It doesn’t. In practice, the assessment develops over several exchanges. If the first report is incomplete or the damage mechanism is misunderstood, that error tends to carry through the whole file unless someone corrects it with proper evidence.

How to Document Your Claim for Success

Good evidence wins arguments before they become formal disputes. Weak evidence forces the owner to rely on memory, and memory isn’t enough when an insurer challenges cause, timing, or extent of damage.

What to record straight away

Start with the obvious. Photograph every damaged area from wide, mid-range, and close positions. Then photograph the paths that connect the damage. If water entered through a roof area and travelled through ceiling linings into walls and flooring, your file should show that chain, not just one stain in isolation.

Keep a written chronology. It doesn’t need legal language. It needs dates, observations, weather event timing if relevant, who attended, what they said, and what changed over time.

Use this checklist as a guide:

- Site-wide photographs: Include external elevations, roof line if visible, gutters, ceilings, walls, flooring, joinery, and any cracking or displacement.

- Video walkthrough: A simple narrated walkthrough helps show relationship between rooms and damage spread.

- Emergency works records: Keep invoices, attendance notes, moisture findings, and photos taken before temporary repairs.

- Maintenance history: Collect prior roof repairs, plumbing works, repainting, waterproofing, or other upkeep records.

- Communications log: Save emails and write down phone calls with date, time, person spoken to, and outcome.

- Replacement and repair documents: Quotes, tax invoices, and previous inspection reports can all become relevant later.

Why maintenance records matter

Insurers often test whether the damage came from a sudden insured event or from wear, ageing, poor maintenance, or long-term deterioration. Owners lose ground when they can’t show the property was reasonably maintained before the incident.

That doesn’t mean every home needs a perfect paper trail. It means any document that shows prior condition can help. Old real estate photos, contractor invoices, renovation records, and dated family photos can all become useful if they show the area before damage.

On site advice: Don’t clean up the story while you clean up the damage. Preserve the evidence first.

For water-related losses, this practical guide on how to maximize your water damage payout is useful because it highlights the kinds of records owners often overlook in the early stage.

What doesn’t work

Some owners submit twenty similar photos of one crack and nothing showing the rest of the room. Others rely on verbal statements from trades with no written findings. Both approaches are weak.

A strong file answers these questions clearly:

| Question the insurer will ask | Evidence that answers it |

|---|---|

| What was damaged? | Labelled photos, room-by-room notes |

| When did you discover it? | Dated chronology and first report |

| What caused it? | Site observations, trade findings, consultant opinion if needed |

| Was it already there? | Prior photos, maintenance records, previous inspections |

| What work is needed? | Detailed scope, not just a lump-sum quote |

Documentation isn’t paperwork for its own sake. It’s the foundation of every later argument about scope, cause, and rectification.

Common Reasons Claims Are Disputed in NSW

A disputed claim usually turns on one of a few recurring issues. The wording changes from file to file, but the pattern is familiar.

Cause of damage is contested

The insurer may say the observed damage wasn’t caused by the insured event. In practice, that often means a dispute about whether the damage came from storm entry, long-term leakage, defective construction, movement, settlement, poor maintenance, or some mix of those factors.

Owners run into trouble with oversimplified reports. A short statement that says “water damage noted” doesn’t explain how the water got in, when it likely entered, whether the failure is isolated or systemic, or what building elements need to be opened up and tested.

The insurer accepts part of the damage, but not the real scope

This is one of the most common practical problems. The insurer may accept a damaged ceiling patch but reject the associated wall damage, insulation replacement, roof rectification, or matching works needed to complete a proper repair. The owner hears “claim accepted” and assumes the issue is resolved. It often isn’t.

A limited scope can leave the owner funding the balance of the repair or living with a patchwork outcome that doesn’t address the underlying failure.

Pre-existing defects are alleged

Where there are older cracks, previous repairs, ageing roof coverings, or signs of prior moisture, the insurer may argue the current damage wasn’t caused solely by the event claimed. Sometimes that position is valid. Sometimes it’s used too broadly.

The key issue isn’t whether the building had any prior age or defect. Most buildings do. The fundamental question is whether the insured event caused compensable damage or materially worsened the condition in a way the policy responds to.

Internal review often doesn’t fix an evidence problem

Many owners assume the next step after an unsatisfactory decision is to complain again in stronger language. That rarely solves a technical dispute. If the insurer’s file already contains an assessment that narrows causation or scope, repeating the same points without better evidence usually produces the same result.

A major practical gap for NSW owners is moving from insurer dispute to tribunal-ready evidence. As noted in this discussion of structural insurance claim assessment, many homeowners don’t realise that independent expert reports are the key to bridging the evidence gap required for NCAT proceedings.

A denied or underpaid claim isn’t only an insurance disagreement. It becomes a building evidence problem the moment you need to prove the assessment is wrong.

When NCAT becomes the realistic next step

NCAT is relevant when the matter stops being a live adjustment issue and becomes a structured dispute about what happened, what work is required, and whose evidence is more persuasive. That shift matters. Informal objections give way to documents, pleaded issues, and expert material that can be tested.

Owners often wait too long to prepare for that step. By then, temporary repairs are done, damaged materials are gone, and the file is built around the insurer’s version of events. If you think the assessment is materially wrong, prepare as if the matter may proceed beyond the insurer’s internal process.

Engaging an Expert for Your NCAT Dispute

The right time to engage an expert is not after you’ve exhausted every internal option and lost months. It’s when you can see the dispute is about technical building issues, not just claim administration.

What an expert report needs to do

A proper Building and Construction Expert Witness Report should do more than say the insurer is wrong. It should identify the property, record the inspection basis, describe observed conditions, separate visible damage from probable hidden consequences where appropriate, address causation from a building perspective, and set out the rectification scope in clear language.

That report must be independent. NCAT won’t be assisted by advocacy dressed up as opinion. What helps is a factual, reasoned report that ties each conclusion to site observations, construction knowledge, and documented evidence.

For owners, lawyers, and builders dealing with a formal dispute, this page on an Expert Witness Report for building matters gives a practical overview of how that kind of evidence is prepared.

Why the Scott Schedule matters

A Scott Schedule is the working document that organises the dispute item by item. It usually sets out the alleged defect, damage, or incomplete work, the claimant’s position, the respondent’s position, and the expert response or recommended outcome.

In insurance-related building disputes, this structure is useful because arguments often become muddled. One side is talking about roof sheets, the other is talking about internal staining, and neither side has linked those items properly. The Scott Schedule forces each issue into a trackable format.

That matters for hearings, settlement discussions, and expert conclaves because it narrows the dispute to identifiable points rather than general dissatisfaction.

What works and what doesn’t

What works:

- Early inspection before evidence disappears

- Clear photographs tied to report observations

- A repair scope that is specific enough to price

- Opinion confined to the expert’s field

What doesn’t:

- Letters that criticise the insurer without technical basis

- Builder quotes with no causation analysis

- Reports that ignore policy-driven dispute points and only list defects

- Late engagement after demolition, drying, or patch repairs have removed the best evidence

Awesim Building Consultants prepares site investigations, Expert Witness Reports, and Scott Schedules for NSW building disputes, including matters that move into NCAT. The value in that work is not the label on the report. It’s the discipline of turning a loose complaint into evidence that can be used.

Frequently Asked Questions for NSW Property Owners

Some questions come up on almost every disputed claim. The answers below are the practical version.

NSW Building Dispute FAQ

| Question | Answer |

|---|---|

| Do I need an independent report if the insurer has already inspected? | If the dispute is about cause, extent, or repair scope, an independent report is often the only way to test the insurer’s assessment properly. |

| Is a builder’s quote enough for NCAT? | Usually not on its own. A quote prices work. It usually doesn’t analyse causation, policy issues, or the technical basis for rectification. |

| When should I organise expert help? | As soon as it becomes clear the assessment is materially incomplete, inaccurate, or unfair. Earlier is better while evidence is still available. |

| Can I recover the cost of an expert report? | That depends on the case, the orders sought, and the outcome. You should get legal advice on recovery prospects in your specific matter. |

| Do deadlines matter in NCAT disputes? | Yes. They always matter. The relevant time limits depend on the type of claim and the pathway used, so don’t sit on the file while trying to negotiate indefinitely. |

| What if I’ve already carried out temporary repairs? | That’s usually fine if they were necessary to make safe, but keep all photos, invoices, and notes showing the condition before and after the work. |

If you’re unsure whether your matter is still a claim handling issue or has become a formal building evidence dispute, get that question answered early. Delay usually makes the proof harder, not easier.

If you need practical guidance on a disputed building claim, contact Awesim Building Consultants. For enquiries about site investigations, Expert Witness Reports, or Scott Schedules in NSW, email admin@awesim.com.au or call 1800 293 746.